You’ve spent years creating value. The next question is how much of it you’ll keep.

Section 1202 of the Internal Revenue Code—known as the Qualified Small Business Stock (QSBS) exclusion—can allow eligible founders and early investors to exclude a substantial portion, and potentially all, of their federal capital gains when qualifying stock is sold.

Recent legislative changes have expanded the opportunity, making tax planning for founders more relevant when raising capital, granting equity, or evaluating future exits.

But timing matters. Many of the decisions that influence QSBS eligibility—including entity structure, stock issuance, ownership planning, and holding periods—are made long before a sale or acquisition is on the horizon.

That’s why Section 1202 is not just an exit strategy. It is a vital component of long-term tax planning for founders and investors looking to preserve flexibility, maximize after-tax outcomes, and turn growth into lasting wealth.

Three Changes That Could Impact Founders and Investors

Recent legislative changes have expanded the benefits available under Section 1202 for stock issued after July 4, 2025. While the rules remain technical, three major updates stand out for those implementing proactive tax planning for founders and investors evaluating future liquidity events.

More Flexibility Around Exit Timing

Historically, shareholders generally needed to hold Qualified Small Business Stock for more than five years before any gain exclusion became available.

The updated rules introduce a phased exclusion structure:

- 50% exclusion after three years

- 75% exclusion after four years

- 100% exclusion after five years

While the greatest benefit still comes from meeting the five-year holding period, the phased approach provides greater flexibility for founders and investors navigating fundraising cycles, changing market conditions, and evolving exit timelines.

Higher Potential Tax Savings

The legislation increased the gain exclusion limitation from $10 million to $15 million per taxpayer for qualifying stock issued after July 4, 2025, with future inflation adjustments.

For founders, early employees, and investors holding highly appreciated stock, the difference can be significant. As startup valuations continue to grow, so does the potential value of proactive QSBS planning.

More Companies May Qualify

The aggregate gross asset threshold increased from $50 million to $75 million, expanding the number of growth-stage companies that may qualify under Section 1202.

However, qualification remains subject to a variety of technical requirements. Understanding whether a company qualifies—and maintaining that eligibility over time—requires ongoing planning and monitoring.

QSBS Planning Starts Earlier Than Most Founders Think

Many founders first think about QSBS when an exit is on the horizon. By then, key decisions around entity structure, stock issuance, ownership planning, and wealth transfer strategies may already be locked in.

That timing can limit opportunities that might have been available years earlier.

Many of the decisions that impact QSBS eligibility are made years before a sale or acquisition. Understanding the planning timeline can help founders preserve flexibility and avoid missed opportunities.

Questions founders should be asking today include:

- Does our current corporate structure support QSBS eligibility?

- Are there ownership structures, trusts, or estate planning strategies that should be considered before significant appreciation occurs?

- How could a future liquidity event affect personal wealth planning?

The earlier these conversations begin, the more flexibility founders typically have when opportunities arise.

Why Investors Are Paying Attention

While founders often receive the most attention in QSBS conversations, angel investors, venture capital investors, family offices, and high-net-worth individuals are increasingly evaluating QSBS as part of a broader investment and wealth strategy.

For investors, QSBS planning may influence:

- Initial investment decisions

- Ownership structures

- Trust and estate planning strategies

- Portfolio construction

- Liquidity event planning

- Generational wealth transfer strategies

As investment gains increase, preserving after-tax returns becomes just as important as generating them.

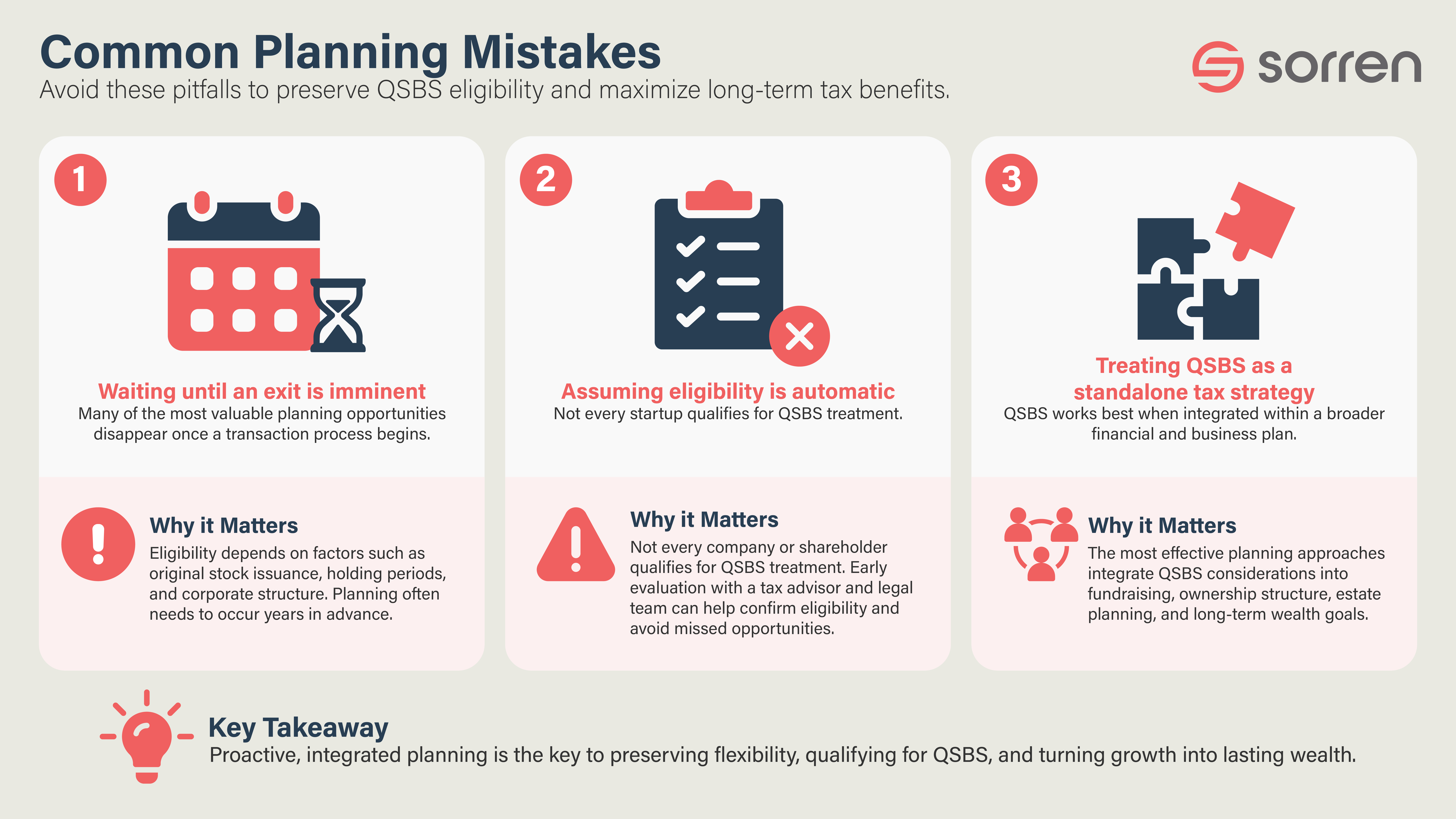

Common Planning Mistakes

Waiting Until an Exit Is Imminent

Many of the most valuable planning opportunities disappear once a transaction process begins.

Because eligibility depends on factors such as original stock issuance, holding periods, and corporate structure, planning often needs to occur years in advance.

Assuming Eligibility Is Automatic

Not every startup qualifies for QSBS treatment.

Eligibility requirements related to business activities, corporate structure, asset levels, and stock issuance remain highly technical and require ongoing monitoring.

Treating QSBS as a Standalone Tax Strategy

The most effective planning approaches typically integrate QSBS considerations into broader conversations around fundraising, ownership structure, estate planning, and long-term wealth goals.

Section 1202 Is About More Than Taxes

The most sophisticated founders and investors don’t evaluate QSBS in isolation.

They view it as part of a broader strategy that connects company growth, fundraising, ownership planning, liquidity events, and long-term wealth creation.

Effective planning often requires coordination across tax, estate, trust, and business planning disciplines—sometimes years before a transaction occurs.

At Sorren, we help founders, investors, and high-net-worth families align QSBS planning with broader growth, liquidity, and wealth creation goals. Because the most impactful planning decisions are often made years before an exit, early coordination can create significantly more flexibility when opportunities arise.

The businesses and investors that benefit most will not necessarily be those with the largest exits. They will be those that began planning early enough to preserve their options.